Since then I have done some research on basket weighting strategy, constituent coins, and operation parameters by making test runs using data from 2013. The discussion was mainly on peercoin.chat .The following are some preliminary results, posted here for better visibility.

The following charts are proof of concept test results using a basket of relatively large cap, long-life coins of mixed technologies. The basket or the three tests are difference due to that less coins existed in older times.

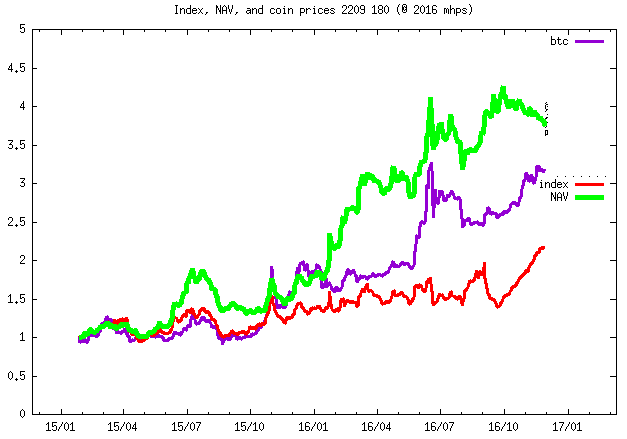

Figure 1

Figure 1 abve is a bull market test (normalized to $1 initial Net Asset Value NAV) from 2015-01 to 2016-11. Btc price (blue) appreciated to 320%; operationally optimized Fund NAV (green) changes to 370%. The Fund out-performed btc by 9.4% in Compound Annual Growth Rate (CAGR). The red curve is the index of minimal variance, which is less volatile than btc price.

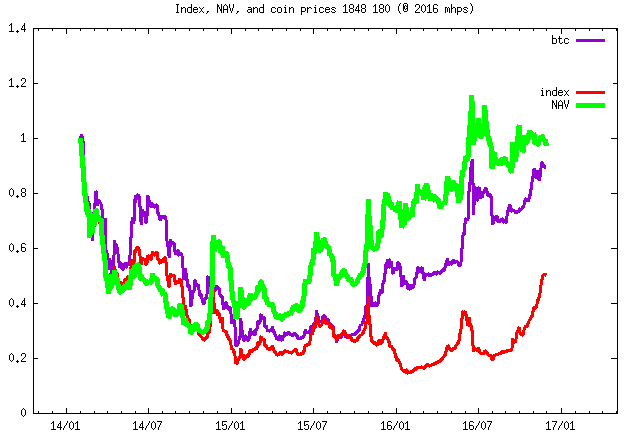

Figure 2

Figure 2 is a recovery market test from 2014-02, after 2013 bubble, to 2016-11. Btc price (blue) changed to 90% the Fund NAV (green) changes to 97%. It out-performed btc by 3% in CAGR

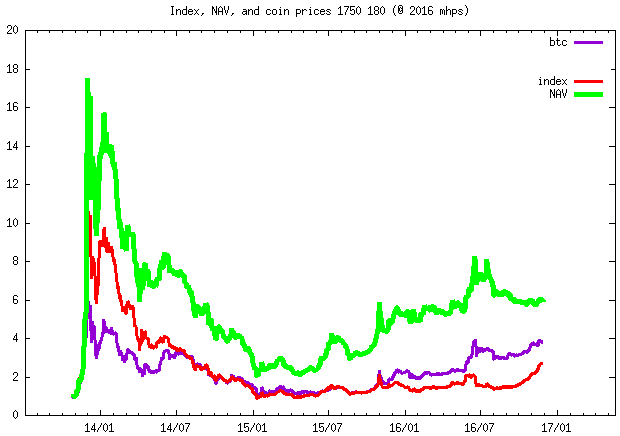

Figure 3

Figure 3 shows a rollercoaster market test from 2013-10, into the 2013 bubble, through its burst, to 2016-11. Btc price (blue) changed to 380%. The fund NAV (green) grew to 590%. The Fund out-performed btc by 15% in CAGR.

As show above, in different market climate the minimal variance index is more stable than bitcoin alone, with the help of a basket cryptocurrencies. Choosing operational parameters can increase return of investment without increasing volatility compared with bitcoin.

That means it’s possible (has been possible in the past) to create a basket of crypto coins that’s more stable than BTC, even though most crypto coins are tied to BTC and tank when BTC/USD surges and surge when BTC/USD tanks.

If it has been possible in the past, it can be possible for the future as well!

If you hold the fund long enough you have good chances to find a point of time when you can sell it at a gain (relative to having kept BTC).

The price in USD is a different matter.

I am still on the fence whether or not should this fund be based in Bitcoin or USD.

Bitcoin is just too volatile and manipulated to be anchored in, but then again majority of markets are most liquid against the Bitcoin.

Both has benefits and drawbacks.

Why not using more than one price - ETF/BTC and ETF/USD?

You (read: the issuing corp) don’t have to trade in both pairs. In fact it would rather be limited to ETF/BTC if you want to keep a liquid reserve in multisig.

The Fund trades all coins with BTC and still becomes stable in USD, because the weights of the constituent coins are determined with their USD prices (crypto/btc x btc/usd ). The USD price is parametric and the Fund does not need to touch a single USD.

The fund holds its constituent coins in the reserve. The value of its reserve, calculated in USD, is the NAV (ignoring liabilities). The Fund trades the altcoints in the reserve with BTC in the reserve according to the algorithm and operational rules formulated based on statistics and optimized by testing. The performance of resulted NAV is shown in the figures.

If the ETF is priced in apples, but you pay in oranges, you might find out that the friction in the apples/oranges trading pair is big enough to make a difference.

All I’m trying to say is that I think it makes sense to use the price of supported trading pairs.

Of course it makes sense to support trading pairs, which are used by everyone, or which have the highest trading volume.